Rightmove (RMV.L)

A monopoly business that is yet to prove itself in a high interest rate environment.

While not really a small-cap by UK standards, Rightmove would definitely be considered small in the US markets. Hence, I will permit myself to write a report on it. Having been one of the most impressive UK growth stories since it’s 2006 IPO, Rightmove has always garnered an expensive valuation. With the stock now sitting at a TTM P/E of 22, is there an opportunity to buy?

Business Overview

If you live in the UK, you’ve almost certainly heard of Rightmove and maybe even used the app. I’m not even in the market to buy a house and yet I find myself occasionally browsing the app just to look at multimillion pound houses. Rightmove has cemented itself as a near monopoly in the property portal business, successfully conglomerating the housing inventory of local estate agents into one nationwide platform.

The company was incorporated in 2000 and the website launched in the same year. With the internet being relatively nascent at the time, the idea of an online property portal, in hindsight, was truly visionary. Rightmove’s business model has 4 pillars with which it generates revenue:

1. Agents pay a subscription fee to advertise their properties and can also pay for additional promotion materials to boost visibility. This also applies to overseas agents targeting British buyers.

2. They sell online advertising space to third parties – such as removal companies.

3. They sell property market data to agents, landlords, surveyors, insurers and mortgage brokers.

4. They sell valuation services.

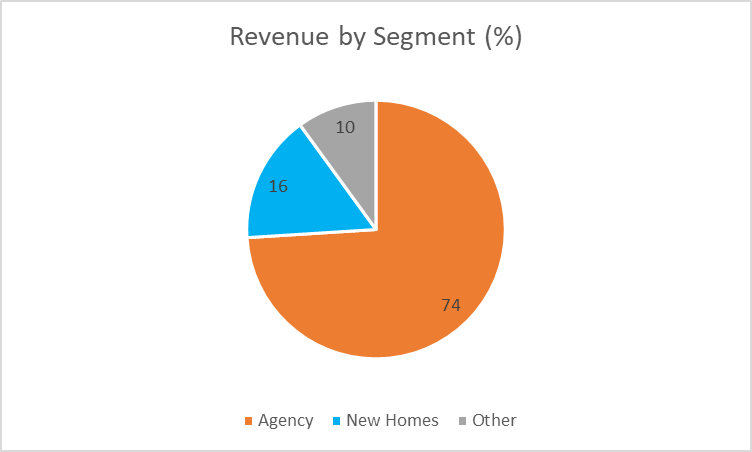

Rightmove doesn’t break down revenue by service.

I believe the key thing that enables these services and what supports the ridiculous profit margins, are what’s known as network effects. Simply put, by having the most popular platform for advertising houses they draw in the most potential buyers which by virtue draws in the most potential sellers, in an ever-perpetuating cycle. Facebook has a similar advantage for advertisers by being the biggest social media platform. Network effects are believed by many to be the strongest competitive advantage a company can have, as they’re extremely difficult to disrupt.

Financial Overview

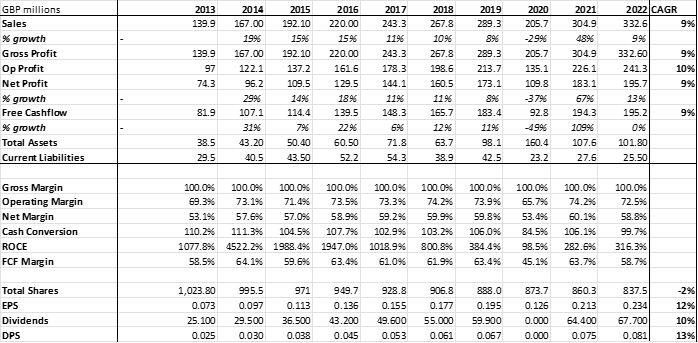

For 2022, revenue grew 9%, in line with the 10-year average, and EPS also grew 9%. Average revenue per advertiser (ARPA) grew 11% but total membership was basically flat on the year, indicating the maturity of the business. The premium service, Optimiser 2020, a package to boost awareness, is now being used by 34% of agents, up from 21%. The question is if the premium service gets to the point where most agents use it, does it not then become the standard? Interestingly, the number of advertisers on the sight dropped from 20,454 in 2018 to 19,014 in 2022, but revenue hasn’t suffered due to the 30% increase in ARPA over the same period.

Rightmove returns practically all its cash to shareholders, with the dividend per share increasing an average of 13% per year since 2013, helped by the fact the company buys back around 2% of shares every year. This is unusual for UK businesses who usually focus on dividend yield.

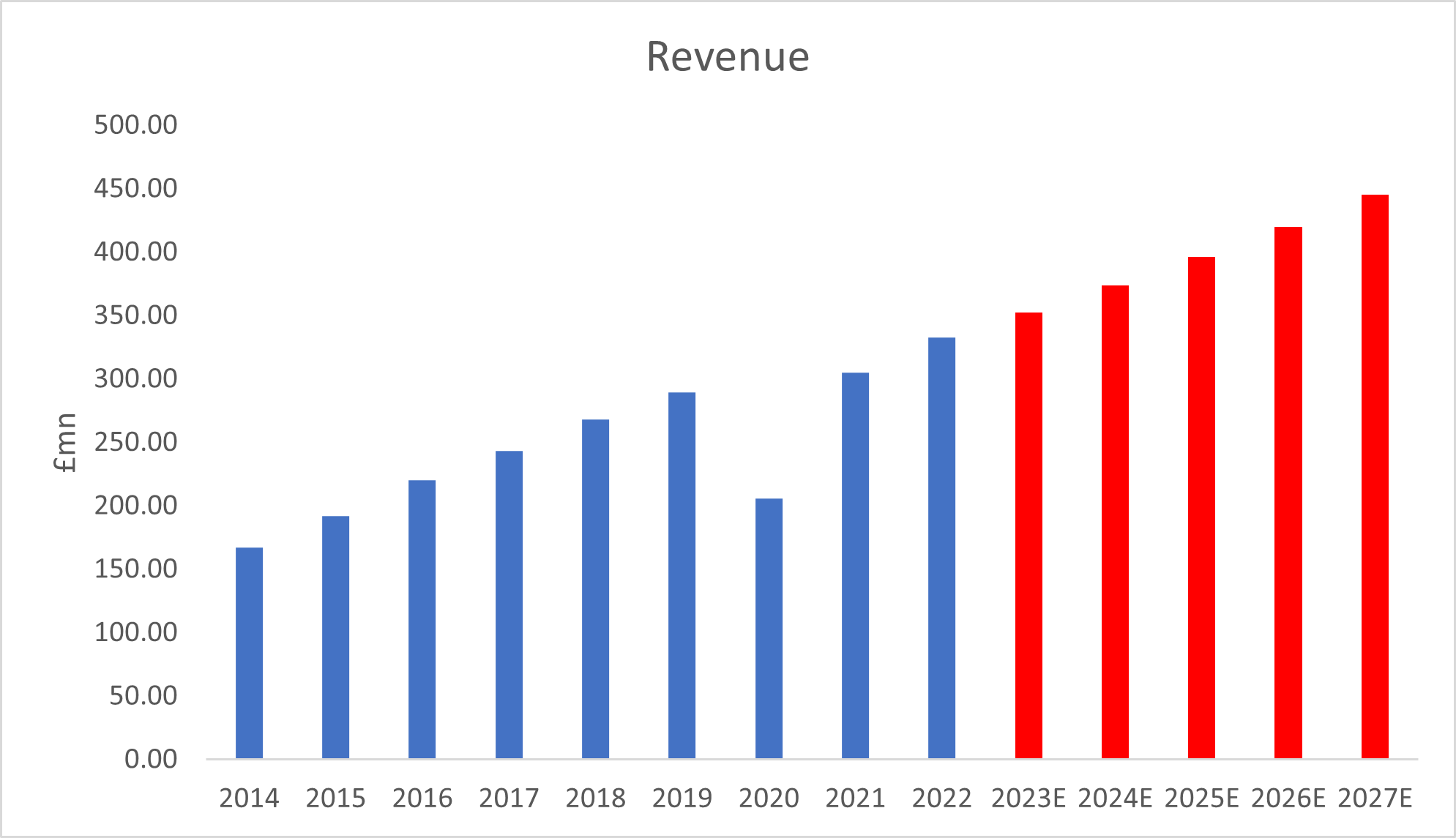

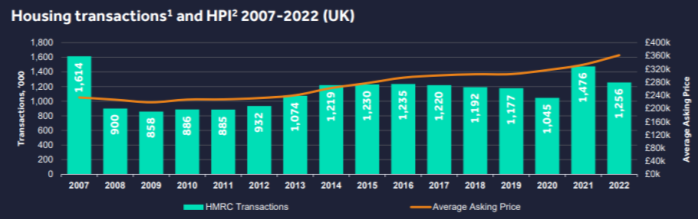

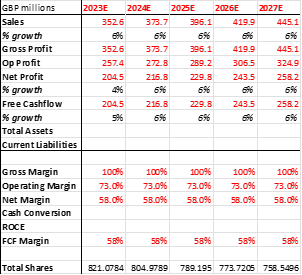

The company’s profit margins are truly incredible with a net margin of 59% and 100% of that turned into cash for the business. Rightmove is also incredibly asset light which means returns on capital-employed (ROCE) are above 100%. This is a business that spits out cash with very little reinvestment. Some would say that reeks of a pure monopoly. As the graph below shows, excluding 2020, revenue grows almost weirdly linearly, built on annual price increases and premium service additions, and is expected to continue to grow around 6% per year for the next 5 years.

As you’d expect, the balance sheet is stellar with £11m in debt and £35m in cash.

Competitors

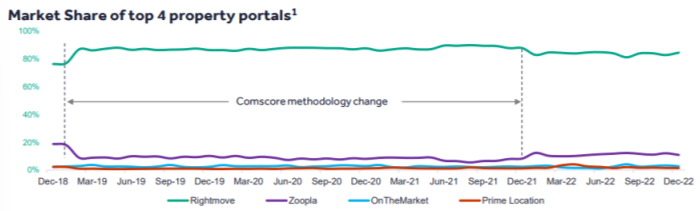

Zoopla – now known as ZPG, Zoopla is the next biggest competitor to Rightmove, but as the earlier graph shows, they don’t have more than an 8-10% market share. Zoopla was bought out by a US private firm for $2.2bn in 2018, a price that seems expensive when comparing market share’s and valuation’s. Zoopla’s USP is that they own a searchable directory of UK residential properties which has allowed them to develop an automated valuation model. The accuracy of estimates is disputed. The only time I ever use Zoopla is to look at previous selling prices of houses.

OnTheMarket – the first time I ever heard of this site was while researching for this report. First impressions are the website seems to be built on WordPress and the pictures of houses are poor quality. Apparently set up by a group of agents who were fed up with Rightmove’s fees, it now has a fee structure that is only 10% cheaper than Rightmove on average. OnTheMarket claims to list houses 24 hours before they appear on Rightmove, “giving you a competitive edge in your search for your next home”, hardly a boast considering buying/selling homes is notorious for being one of the slowest, most painful ordeals you can experience in life.

PurpleBricks – while not directly a competitor as it is an online estate agent, PurpleBricks lists their properties on places like Rightmove and Zoopla and operate a no-sale-no-fee policy. The share price chart below shows you all you need to know about PurpleBricks. The company was recently sold for £1 after burning through £20m of cash in 2022 with negative operating profit and £33m in liabilities. A true fall from grace.

Risks

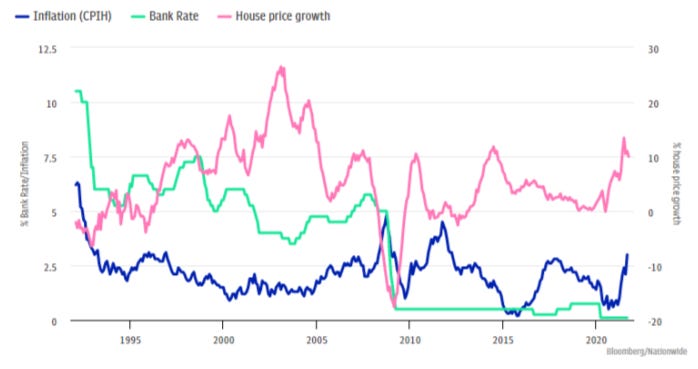

Economy and Housing Market - My biggest qualm with buying Rightmove, even with it sitting at a historically low P/E of 22, is that barring the 2007-2009 period, which of course contains the GFC, the company has never operated under a high interest rate environment.

Post GFC, the average UK house price has risen from £160k to £290k. Rightmove have almost certainly benefitted from the prolific buying and selling of houses that has occurred in the last decade, a period where mortgage rates have spent most of the time below 3%. The average 5-year fixed mortgage rate has risen from a low of 1.3% in 2021 to 4.6%. Logic tells me, this means people looking to re-mortgage are going to face massively increased payments. For the individuals who can absorb this extra cost it’s not a big issue. Those who can’t are going to look to sell and downsize which ultimately leads to a glut of sellers on sites like Rightmove. But of course, this sudden increase in rates means people aren’t looking to buy. I expect many will be waiting on the sidelines in the hope that rates are cut again. With UK inflation still rampant and the BoE notoriously slow to react compared to the US, there’s definitely further rate increases in the pipeline.

According to Capital Economics,

“When the Bank Rate was at 0.1pc, a homeowner spent 38% of the median income to service an 80% mortgage on an average priced home – or £827 per month. When the Bank Rate rose to 1.75% in August 2022, a buyer had to pay 45.5% of their income towards their mortgage.”

With the base rate now at 4.5% the percentage of income homeowners are spending on their mortgage is likely much higher. The last time mortgages were this expensive the average house cost 5.2 times average earnings whereas today the ratio is 6.8, say Nationwide.

Being the force that they are within the UK housing market, Rightmove collects their own data. Their 2022 results presentation expressed that even with rates rising, neither housing prices nor transaction volumes had decreased, but I think 2023 will give a fairer representation of the current environment, being that rates are much higher than they were at the end of 2022.

Ultimately, I feel that a quiet housing market would make it difficult for Rightmove to push their consistent price increases onto agents and new premium products would receive less uptake, potentially stunting growth for a few years. However, the board say they’re confident in Rightmove’s performance for 2023 so we’ll see.

Competitors – I currently don’t see any competitors as threat nor do I see how any new entrants could steal market share. Cost advantages aren’t advantages when they come with less eyes looking at adverts. Zoopla’s selling point of giving value estimates seems redundant now that Rightmove offer ‘Track My Property’ with their own estimates.

Regulation – One aspect that surprises me is the lack of any noise from the CMA on a company that clearly shows signs of being a pure monopoly. There is definitely potential for future regulatory uproar and at the same time, I’m unsure how Rightmove would be dealt with. When customers choose to use a service because it is the best at what it does, you can’t force them to use an inferior service in the name of ‘preventing a monopoly’. I refer to Google as an example.

Valuation

The 10Y key financials model is above. My estimates for the next 5 years of growth are below.

DCF Method –

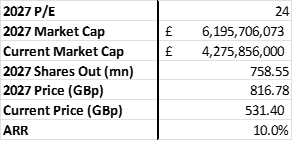

Using a blended EV/EBIT and perpetual FCF growth method with a 2027 final multiple of 16 and perpetual growth rate of 2.5%. Weighted-average cost of capital is around 8%. The price target comes out to 547p, around 3% above current prices, leaving us no real margin of safety.

Future P/E Multiple Method –

Approaching from a different angle and using historical P/E multiples.

Rightmove has always had a relatively high multiple even though the business has been ‘mature’ for several years. Whether the multiple is warranted depends on what you think the potential is for continued growth.

Based on history, the current 22 P/E reflects relative negativity surrounding the company. I have used a 24 P/E in 2027 in anticipation of a strong/normalised housing market, lower interest rates and continued mid-single digit growth. I have continued the 2% annual share count decline along with the same earnings estimates as above.

We get an estimated annual return of around 10%.

Conclusion

Rightmove is clearly an impressive company with many of the aspects you’d look for in an investment. I think that the business could continue growing at low single digits, which combined with the dividend and share buybacks could turn it into a serious cash cow. However, I am hesitant about investing due to an uncertain housing market that seems destined for bloodshed. I also think that if growth does fail to materialise then the current high P/E has potential to contract considerably.

The potential for future CMA focus is a good one, but I think rn they are focused on mergers and acquisitions rather than monopolies from growth.

Do you have views of Rightmove's moat compared to its competitors, and the level of insider ownership?